When Is It a Good Idea to Take the House Off the Market and Relist Again

As we finally come out of the pandemic, the housing marketplace has turned hot. Demand is extremely stiff from first-time homebuyers, trade-up buyers, and institutional investors. Simply there's a chance the housing market place is likewise hot. Therefore, information technology's worth worrying about the housing market place again.

If y'all program to buy a house, you should also think about what could go wrong. This manner, yous won't go blindsided in case things practise. Think about all the people who bought real estate in 2007 and early on 2008. Things were going wonderful, then the global fiscal crunch hit! If they had to sell before 2012, they probable lost money.

With the South&P 500 and NASDAQ selling off at the first of 2022, existent estate investors should take note. There's a run a risk the housing market could fade equally interest rates rising. The Federal Reserve could tighten as well much, also often, and cause a recession.

For the record, I am withal bullish on the housing market place over the next several years. The millennial generation is in total ownership mode. Inventory and mortgage rates will remain low. Meanwhile, foreigners are likely going to flood the U.Southward. existent manor market again after ii years of existence shut out. Simply like any good investor, it'due south practiced to meet the other side of the story.

A Slowdown In Housing Is Inevitable

The footstep of house price growth will boring considering information technology cannot outpace income growth past such a broad margin for too long. Bond-tapering and Fed rate hikes started on March 16, 2022. Meanwhile, house prices are high. Affordability is becoming an result.

This pace of double-digit price appreciation in the housing market is unsustainable. Instead, I think home prices will rise by closer to 8% in 2022, not xvi% like it did in 2021.

Let'south go over some more details on why the housing market has some signs of concerns. With such concerns, yous may want to invest in a publicly-traded REIT or a private eREIT from Fundrise, instead of ownership a single asset with a big mortgage. Diversification is key in this hot market.

Why We Should Start Worrying Almost The Housing Market

Taking on massive debt to buy existent manor at record highs is risky. You demand to be sure you're following my 30/30/3 habitation buying rule before proceeding. If yous follow my rule, you will significantly increase your chances of beingness able to comfortable beget your home.

Let's say you lose 50% on your stock and bail portfolio. You lot'll be upset, merely be fine. If your property loses 20% of its value, however, this ways yous've lost 100% of your 20% downpayment.

Below is the latest U.Due south. house growth chart from January 1976 to June 2021. According to the Freddie Mac House Price Index, firm price growth is at an best loftier. Noice the previous all-fourth dimension loftier house price growth in the late 1970s and in 2006.

If you are buying belongings today, yous need to be prepared for a potential rapid deceleration in prices. Therefore, you must purchase property strategically if you do purchase.

In this scenario, you'll besides probably nevertheless be fine – if yous don't accept to sell. But when property prices right by twenty% or more, many people become forced sellers considering they've too lost their jobs.

I empathise that millennials are coming of buying age and inventory is on the decline, making competition for buying a dwelling house fierce. However, only if you are fully cognizant of the following points I've highlighted below should you go on with a property purchase today.

Things To Know Before Ownership Holding Today

Before yous purchase one of the biggest assets in your life, it'south proficient to know the electric current marketplace condition. It'south also proficient to know what could go incorrect in the housing marketplace.

1) Rents softened, but are recovering

Given property prices are a function of rental income multiples, a real estate buyer should be looking to buy at similar pricing discounts from top rental periods.

Rents softened in major cities such every bit New York City, San Francisco, Seattle, and DC due to the pandemic. However, I anticipate rents to rebound once we attain herd amnesty. But they may not as people scatter to lower price areas of the country.

Pay very careful attending to the latest monthly rental figures earlier buying property. Home prices accept increased while rents softened in 2020. Therefore, the valuation for home is much higher. Rents need to aggressively rebound by 10% or more in 2021 and beyond in many major cities for valuations to return to normal.

2) Mortgage manufacture is however very tight

Here'south what's going on in the mortgage industry, which is as stringent as it has ever been. Only people with 720+ credit scores and 20% downpayment have been able to go a mortgage. This is good in that a fallout is less likely in the future. But permit's talk about some concerns.

Liquidity (Profitability) Concerns: A growing percent of people are not paying their mortgages and banks are uncertain if and when payments will resume. As a result, his banking company is only lending to the well-nigh financially fit customers.

Stricter Lending Standards: Due to liquidity (profitability) concerns, banks have significantly tightened lending standards. Here are some of the increased lending standards he mentioned to me dorsum in 2020:

- Temporarily stopped allowing for cash-out refinances

- No longer fully counting RSU values when calculating how much a person can borrow

- Schedule E income (rental income) when calculating how much a person tin can infringe is no longer included

- No longer approving Dwelling house Equity Lines Of Credit (HELOC)

- Minimum downpayment is 20%

- Raised minimum credit score to authorize for a mortgage to 680

In other words, lending standards are as strict as it gets. As a result, perchance there is upside to real estate liquidity if there is a reversion to pre-pandemic level standards sooner. Only if lending standards go on to tighten, it may squeeze out the marginal heir-apparent in the brusk-term.

iii) Mortgage rates are finally creeping higher

Mortgage rates hit tape lows in 2020. At present, mortgage rates are on the rise as bonds sell off and expectations for inflation is high.

My last mortgage refinance was in 4Q2019 when I locked in a 7/ane ARM jumbo ARM at 2.626%. I was pumped! Withal, today, that same rate might be at two.875%. The average 30-year fixed-rate mortgage is closer to 3% today.

The problem with record-low mortgage rates is that thousands of Americans are tempted to buy besides much house. Americans are violating my xxx/30/iii abode ownership rule, which puts the future housing marketplace in jeopardy.

Notice how mortgage rates have soared in 2022. The average thirty-twelvemonth fixed charge per unit mortgage is back to about 5%. Still low by historical standards, but more than than 1% higher than mortgage rates were in 2021.

Higher mortgage rates in 2022 is the biggest reason to worry virtually the housing market once again. Higher mortgage rates WILL dull downwardly the housing market place, which is why you shouldn't get into crazy bidding wars. That said, I notwithstanding think prices will increase in 2022 due to undersupply.

4) Prices have surpassed their previous peaks in many cities

While every city is different, if you look at the prices in Denver and Dallas, you lot'll find that the prices are roughly 45% higher than they were in 2006-2007. This toll operation is similar to San Francisco's. Meanwhile, hot cities like Seattle and Portland are simply nigh 20% to a higher place previous peaks.

The U.s.a. median existing home price is about 40% higher than its previous pinnacle in 2007. Nosotros're talking nigh a median existing habitation price from $250,000 in 2007 to $400,000 today. That's significant. But then again, 14 years have passed. As a real estate investor, your goal is to invest in markets that have both underperformed and take the potential to take hold of up.

five) Revenue enhancement reform takes time to negatively impact housing prices.

Conceptually, we all know that limiting state income and property tax deductions to $10,000 and limiting mortgage involvement deductions on new mortgages up to $750,000 are net negatives for expensive coastal city real estate markets. Yet, information technology takes one-2 years to start feeling the crunch of revenue enhancement reform.

Think nigh information technology. Permit's say you own an average iii bedroom, 3 bath home for $i.5 million. Your property taxes alone toll $17,000 – $xx,000 a year, depending on which state you reside.

Permit's say you earn $120,000 a year. Yous'll accept paid $6,000+ in state income taxes. In the past, yous could have deducted the entire $23,000 – $26,000 from your income. Now, y'all are limited to $10,000 in deductions.

Some volition argue that lower income taxes will showtime these deduction limitations. Maybe.

With Joe Biden as President, a whole host of new taxes could be increased or introduced. Given the government is in such a massive deficit, college taxes or cuts to resources are an inevitability. Tax reform is a headwind, not a tailwind for coastal city property price appreciation.

6) Inventory is slowly creeping higher

The structure blast we've experienced over the past several years is finally showing up in the data as a wave of new inventory hits the marketplace. When there'southward more inventory, pricing comes under pressure level if demand doesn't follow. Below is the latest housing inventory under construction and authorized, but not started.

Hither is a another inventory of single family unit homes chart that showed what happened once the pandemic began. Even so, as of 2Q2021, inventory seems to have bottomed out and is likely going to go back upwardly again. Therefore, expect to run into more opportunities in 2H2021 and 2022 at the margin.

Hither's another latest housing inventory chart by Altos Research. Equally you can see, housing inventory bottomed in April 30, 2021 and has steadily risen until this twenty-four hour period. Housing inventory is even so way below normal. Even so, information technology's good to keep an eye on inventory given prices are also much higher.

For some of the hottest cities for real estate, like Austin and Nashville, inventory is definitely creeping higher. If inventory gets too high, these heartland cities are at take a chance of a housing downturn. Accept a expect at this nautical chart below that shows single-family permits way up for Austin, Dallas, and Nashville.

Personally, I wouldn't be investing in cities in the acme-right quadrant. Instead, I would be investing in cities in the greenish, lower-right quadrant. You lot don't really desire to invest in markets where habitation prices rose the most while likewise facing the nearly amount of increasing supply.

7) It takes a while to recognize a height.

The housing boom that began in Jan 1996 ended in March 2006. But it wasn't until the commencement of 2008 that people started to accept that the housing market had already peaked.

Until 2008, belongings investors were still clinging to hope or at least were in deprival that prices would no longer be going upwardly. In one case Acquit Sterns was sold for nothing to JP Morgan in March 2008, people started to panic.

Then Lehman Brothers went nether on September 15, 2008, a full two and a one-half years afterward the housing market peaked. And things got fifty-fifty worse, with the Southward&P 500 finally bottoming out on March 9, 2009. At least as of 3Q2020, we already experienced an aggressive 32% decline in the South&P 500 in March 2020.

Below is a great chart that shows how badly housing prices corrected in some of our major cities. Notice how the previous boom lasted 10 years and the crash lasted 5 years. Therefore, 20221 could be the height in the current housing smash and we don't fifty-fifty know information technology for several more years.

8) The stock marketplace has crashed multiple times

We saw a tearing 20% sell down in the S&P 500 in 4Q2018. Then nosotros saw a 32% decline from peak-to-trough in the S&P 500 by March 23, 2020. The S&P 500 and the NASDAQ corrected by 10%+ in 2022 already. Every bit a result, investors need to scout out.

From policy errors past the Fed, to trade wars, to slowing global growth, to a potential war with Islamic republic of iran, to COVID-19, to a global pandemic, companies everywhere will be more cautious on their spending in 2022 and beyond.

Just know that prices tend to revert dorsum to the mean or overshoot on the downside very iv – 10 years. Real manor takes 2-5 years to right, so there is no rush to buy now.

I'm predicting very mediocre S&P 500 returns for 2022. We could easily shut the year down. So far, the Southward&P 500 is struggling in 2022 and the NASDAQ entered bear market place territory.

Recognizing Signs Of Housing Marketplace Strength

Although it's skilful to worry about the housing market again, let us also recognize that the housing market has continued to rebound. The reasons are:

- Low mortgage rates and negative existent mortgage rates.

- The Due south&P 500 airtight up 18% in 2020 and up 27% in 2021.

- A rotation out of volatile stocks into more stable existent estate

- Still not enough inventory

- The increased desire for income / yield

- Demand from institutional real estate investors competing against retail investors.

- Foreign buyers will probable come up back to the Us in 2022+ with over $200 billion in pent-upwards demand

Purchase Real Estate Responsibly

The mass media and the real estate industry will focus on strong demand, strong job growth, and a dearth of inventory as drivers for higher belongings prices in 2021 and beyond.

That'south fine if you tin surgically buy in potent task cities via real manor crowdfunding. The heartland of America is an especially attractive area to buy. Valuations are much cheaper and net rental yields are much higher. At that place should exist a multi-decade trend of spreading out across America thanks to technology.

Still, in that location are more deals to be had in expensive littoral cities like New York and San Francisco also. Big cities are making a strong comeback and accept lagged the overall U.Due south. real estate market place during the pandemic.

If you lot're dying to buy a primary residence today, make sure you can withstand a 10-20% correction over a five year fourth dimension frame. It'south always good to plan conservatively. I don't call back the housing market place will crash in the adjacent three years. In fact, I call up we'll boilerplate loftier single digit gains through 2024.

If y'all don't take a financial buffer equal to at least x% of the value of your holding later on putting downwardly 20%+, then y'all are not financially prepared for a downturn. You need to try and buy at a price that is at least 5% lower than the previous comparable sale toll.

Too much debt is really what will kill you if nosotros ever return to hard times. Buy a house to bask life instead of looking to brand a profit. As presently as you lot commencement hearing regular reports about people putting no money downwards, then information technology will be really time to worry virtually the housing marketplace. But for now, real estate is likely going to continue going up every bit global economies reopen.

Build Wealth Strategically Through Existent Estate

Real manor is my favorite way to achieving financial freedom because information technology is a tangible asset that is less volatile, provides utility, and generates income. Stocks are fine, but stock yields are low and stocks are much more than volatile. The -32% decline in March 2020 was the latest example. However, real estate held steady and appreciated in value then.

Investing in existent manor crowdfunding is a solution for variety and exposure. Instead of taking on a mortgage to buy existent estate, you can merely invest in a diversified private eREIT through a firm similar Fundrise. If you don't have the downward payment or desire to bargain with tenants, investing through Fundrise is a hassle-costless style to make passive income.

If you are a real manor enthusiast who likes to invest in private deals, check out CrowdStreet. CrowdStreet focuses specifically on real estate opportunities in 18-60 minutes cities where valuations are lower and rental yields are college. The spreading out of America is a long-term trend thanks to technology.

I've personally invested $810,000 in real estate crowdfunding across 18 projects to take advantage of lower valuations in the heartland of America.

My real estate investments account for roughly 50% of my current passive income of ~$310,000. To exist able to earn income 100% passively every bit I take intendance of my two young children is a dream come true.

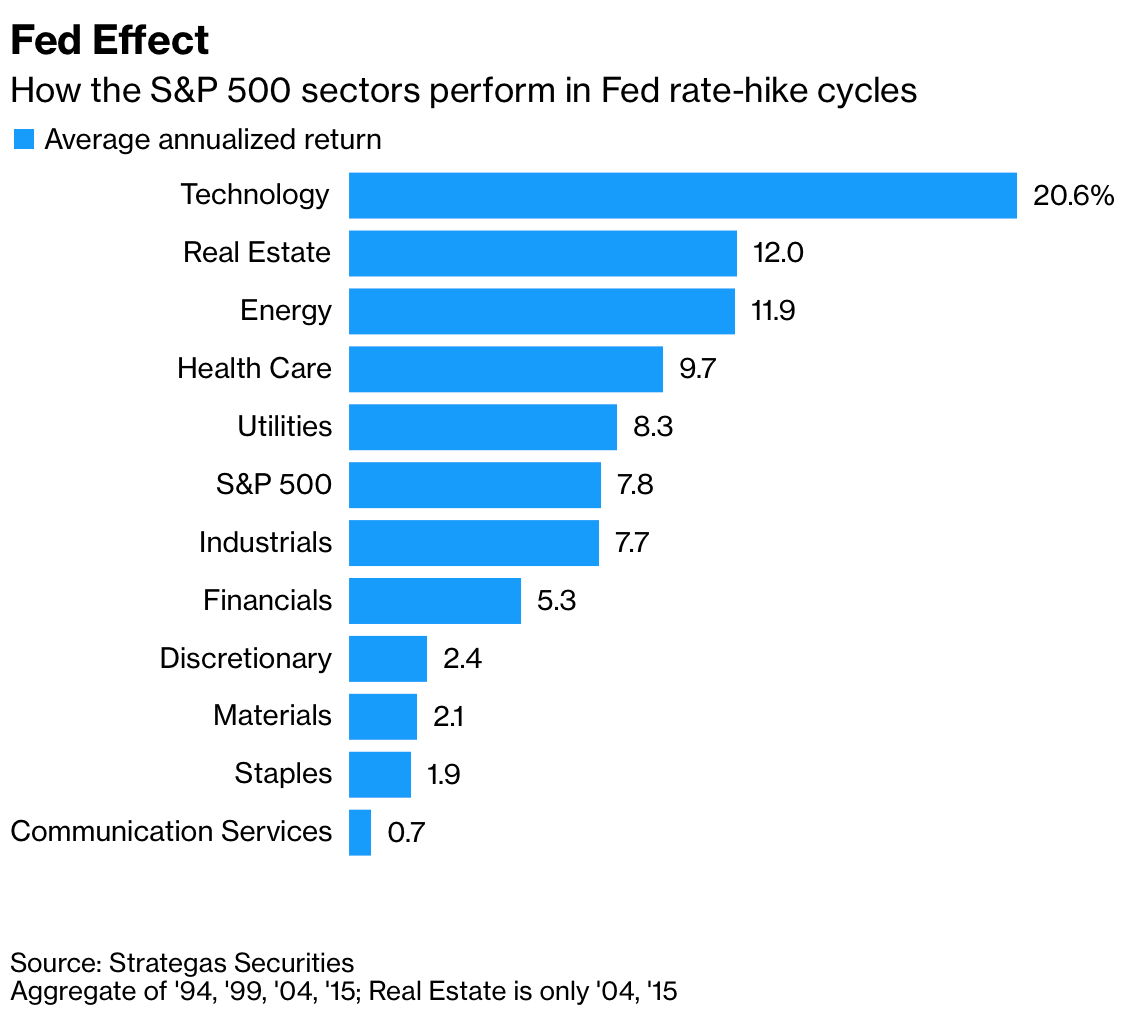

Below is a great nautical chart regarding how existent estate performs after previous Fed rate-hike cycles. Peradventure surprisingly, real estate performs very well considering rising rents more than offset higher mortgage rates.

Refinance Your Mortgage

Cheque out Apparent, my favorite mortgage market where prequalified lenders compete for your business organisation. You lot tin can get competitive, real quotes in under 3 minutes for gratuitous.

Mortgage rates are nonetheless near all-time lows, but they might start ticking upwardly due to inflation. Take advantage and lock in a generationally low mortgage rate today. I was able to get a 7/1 ARM for 2.125% with naught fees for a new forever habitation I bought in 2020.

Purchase The Best Selling Personal Finance Book

If you want to drastically improve your chances of achieving financial liberty, buy a difficult re-create of my new book, Buy This, Not That: How To Spend Your Way To Wealth And Liberty. The book is jam packed with unique strategies to assist you build your fortune while living your best life.

Purchase This, Not That is already a #1 new release and #i all-time seller on Amazon. By the time you terminate BTNT you volition gain at least 100X more value than its cost. After spending 30 years working in finance, writing about finance, and studying finance, I'g certain y'all will honey Purchase This, Not That. Thank you for your support!

It's Time To Start Worrying Well-nigh The Housing Market Once again is a FS original mail service. I've been a real estate investor since 2003 and ain multiple properties today. Stay alert and bargain difficult! Consider writing a toll concession letter if you have to. Whatever information technology takes to get the best deal possible.

Source: https://www.financialsamurai.com/time-to-start-worrying-about-the-housing-market-again/

0 Response to "When Is It a Good Idea to Take the House Off the Market and Relist Again"

Post a Comment